In a small village in Burkina Faso, Alphonse launched a café with just 300 000 Fr (CFA frances, XOF, equivalent to ~450 €) in funding from a friend abroad — all structured through the FlexUp platform. With no legal entity required, he set up contracts between himself, the investor, and the landlord, using FlexUp’s flexible model to split payments into firm, flex, and credit tranches.

Within a year, the café reached profitability, fairly distributing revenues, repaying part of the investment, and building equity stakes for all contributors based on their risk and effort. Café Alphonse shows how even the smallest ventures can become transparent, investable, and collaborative with the right tools.

🔎 Highlights

- Type: ✅ Real case study

- Country: Burkina Faso

- Project type: Small café

- Team size: 1 – entrepreneur

- Associates: 3 – entrepreneur, investor, landlord

- Legal structure: Subaccount under Alphonse's Personal Account

Context

Alphonse is a young entrepreneur living in Burkina Faso who dreams of opening a small café in his village. He needs an initial capital of 300 000 Fr to purchase equipment and stock groceries. His revenue forecast starts at 100 000 Fr per month, growing by 10 000 Fr each month. Groceries are expected to cost 10% of revenues.

Alphonse shares his idea with Bernard, a friend from France, who agrees to invest. Bernard is willing to provide the initial funding but expects Alphonse’s salary to be paid from the café’s revenues.

Alphonse has already found a suitable location and has a good relationship with the landlord, who asks for 40 000 Fr/month in rent but is willing to be flexible at the beginning as the business gains traction.

Bernard proposes using the FlexUp platform to properly structure the project and allow a flexible remuneration scheme and full transparency for all parties involved.

Deal structure

Alphonse's target remuneration is 75 €/month, with the following payment structure:

- 25 000 Fr paid in cash (33% Firm)

- 25 000 Fr paid as a flexible remuneration (33% Flex)

- 25 000 Fr invested in the project (33% Credit)

The rent of 40 000 Fr/month is split as follows:

- 30 000 Fr paid in cash (75% Firm)

- 10 000 Fr paid as a flexible remuneration (25% Flex)

Bernard invests 300 000 Fr, entirely allocated as credits (100%).

They also agree to create a base reserve, gradually saving up to 100 000 Frfrom revenues, to cover future firm expenses.

Payment priorities are structured as follows:

- Firm tranches must be paid in all cases, regardless of profitability – otherwise, the project is in default (which could, for example, terminate the lease).

- Flex payments are made only if sufficient cash is available at the end of the month, after paying all firm expenses and after the base reserve is fully funded.

- Credit payments are not paid out monthly – instead, they are reinvested into the project and paid back later if surplus cash is available at the end of the year.

Flex and credit tranches involve varying degrees of financial risk – 20% for flex, and 80% for credit. To compensate this, each associate receives tokens based on the risk-weighted value of their contributions. Tokens grant voting rights and a share of any profit distributions.

Setting up the business

Alphonse signs-up up to the FlexUp app, creates his personal account, then creates a “Café Alphonse” subaccount (i.e. a project owned by him, without a dedicated legal entity). He then signs the FlexUp Charter for the Café Alphonse account, and sets up contracts with himself (for services), the landlord (for rental), and the investor (for funding). All documents are generated and signed electronically via app on his mobile phone.

He receives the funds, purchases equipment and groceries, installs the café, and launches operations — all in just a few clicks, no paper work involved !

Outcome

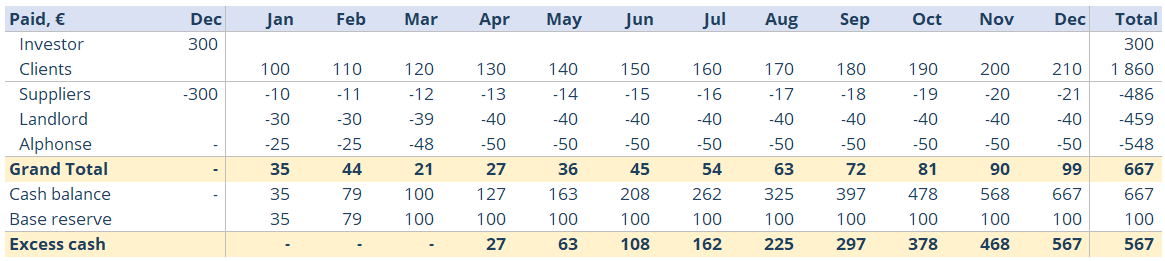

Cash Flow Summary (Year 1):

- By the end of March, the base reserve had reached its target of 100 000 Fr.

- From April onward, Alphonse’s firm and flex remuneration and the full rent were paid.

- By year-end, the café generated 1 860 000 Fr in revenue and accumulated 567 000 Fr in excess cash.

This cash was distributed:

- 50% to credit buyback, pro-rata each associate's credits,

- 50% as profit distributions, pro-rata each associate's number of tokens

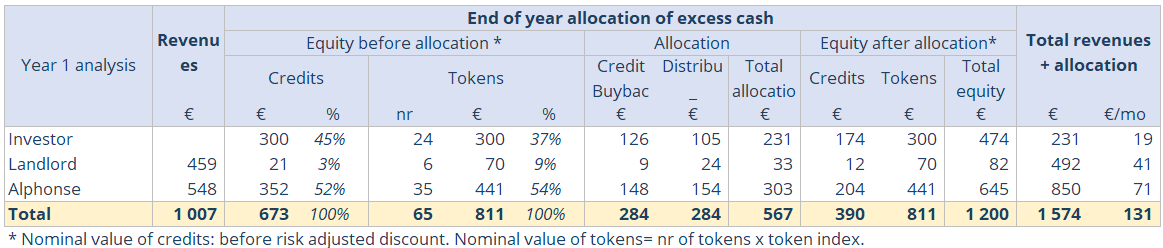

Resulting Positions:

- Alphonse received 850 000 Fr in total cash (monthly remuneration + profit share), equivalent to 71 000 Fr/month. He also built 645 000 Fr in equity, and now holds 54% of the tokens, gradually increasing his stake as the business grows.

- Bernard recovered 231 000 Fr of his initial investment and holds 474 000 Fr in equity. He can expect full credit recovery and more distributions next year and may choose to exit through a future token buyback.

- The landlord earned 492 000 Fr – exceeding his base rental income – and acquired 82 000 Fr in equity.

The project was easy to launch, economically viable, and achieved fair, transparent sharing of profits based on the contributions and risks of each associate.

What benefits did FlexUp provide?

Bernard and the landlord both believed in Alphonse’s potential but had no practical way to support him within the constraints of traditional economic systems:

- Formal economy: Setting up a legal entity for such a small venture would have been too costly, slow, and complex — exposing Alphonse to administrative burdens and potential arbitrary obstacles.

- Informal economy: Like many small businesses in Africa, informal operations lack legal clarity, making collaboration insecure and limiting trust between stakeholders.

This is why Bernard recommended FlexUp:

- It’s incredibly easy to set up – just a smartphone and internet connection are required.

- It provides unmatched flexibility to create tailored financial arrangements, such as splitting payments into firm, flex, and credit tranches.

- All associates have real-time access to the café’s transactions, ensuring transparency and fostering trust.

- The system generates all contracts automatically using standardized templates, removing the need for costly legal advice or complex negotiations.

Conclusion

Café Alphonse demonstrates how the FlexUp platform enables micro-entrepreneurs to structure and launch projects that would otherwise remain informal and unable to attract investors and business partners.

Thanks to FlexUp, Alphonse turned a 300 000 Fr investment into a thriving business with shared governance, equitable returns, and growing long-term value.

The success of Café Alphonse proves that small-scale projects can become structured, resilient, and scalable – opening the door to a new, more inclusive and flexible economic model.

🔗 Explore further

- 📄 Download the full case study – Café Alphonse Use Case.pdf

- 📊 Download the financial model – Café Alphonse BP.xlsx

- 🧪 Log into our demo site to view this use case in the FlexUp app:

- Link: demo.flexup.app/login

- Email: cafe@example.com

- Password: demo

Discovery other use cases

Café Alphonse