Introduction

In Africa's renewable energy sector, the conversation often revolves around the lack of capital or weak infrastructure. But another, less visible obstacle is just as significant in blocking the transition: the infamous "valley of death," the critical phase where projects die for lack of funding before they even reach maturity.

Few people understand this challenge better than Fabrizio Nastri. With over 25 years of international experience in the energy sector – from Shell to Arcelor, and through the Boston Consulting Group and Canopy – he has closely observed the limitations of the current system on the African continent.

Today, with the launch of FlexUp, he is proposing an innovative approach to rebalance the distribution of risk among developers, investors, and bankers, giving African solar projects a real chance to reach the finish line.

In this exclusive interview, he shares his vision, his diagnosis, and how FlexUp can help unlock the continent's solar potential.

1. How did the idea for FlexUp come about?

"Actually, the idea for FlexUp came directly from my own entrepreneurial journey. I have over 25 years of experience and have founded several companies, particularly in the solar energy sector in Africa. I had a company called Canopy, with five subsidiaries on the continent, and unfortunately, it went bankrupt due to financial conflicts of interest between our clients, suppliers, banks, investors, employees, and the directors of our subsidiaries.

After that failure, I took a year-long sabbatical to reflect. I told myself that it was absolutely necessary to invent a system that avoids these problems and truly facilitates business development, especially in contexts like Africa. On one hand, Africa has an informal economy with very few legal protections and a lot of uncertainty for entrepreneurs, which excludes them from bank financing and hinders business development. On the other hand, the formal economy is so administratively burdensome that it discourages many people and can stifle startups.

FlexUp was born from this desire: to provide a flexible, fair, and transparent model that removes these blockages and allows entrepreneurs to collaborate without discrimination, sharing risks and rewards in a clear manner."

2. What are the differences compared to classic financing?

"In the classic financing system, we face a binary model. On one side, you have the bank (debt financing), which wants to take no risk and demands guarantees and maximum visibility on your revenues. If you can't repay, you go bankrupt. And if you succeed brilliantly, the bank gains nothing extra; it has no 'upside.'

On the other side, you have investors (equity financing), who take on more risk but also take control of the company and capture the majority of the profits in case of success. This dichotomy leaves little room for intermediate solutions.

FlexUp eliminates these distinctions. In our model, there is no longer a rigid separation between debt and equity – or even a distinction between labor and capital. Any participant – banker, investor, supplier, client, employee – can contribute to the project's financing and be compensated through a common mechanism.

Everyone freely chooses their level of risk and can distribute their compensation across three levels:

- Firm (low risk): Must be paid on schedule, just like in the classic system.

- Flex (intermediate risk): A monthly payment adjusted based on available cash, after 'Firm' commitments are paid.

- Credit (high risk): Deferred compensation, paid annually based on profits.

The higher the value of your contribution and the more risk you take, the more 'tokens' you receive. These tokens give you voting rights and a share of the profits.

This unique and transparent system applies to all stakeholders. It aligns financial interests, encourages collaboration, and allows for a fairer distribution of the created wealth."

3. What are the main benefits for an African solar project developer?

To answer precisely, we need to distinguish between the two major phases of a project: the development phase and the implementation phase. FlexUp brings decisive benefits to both.

Source : World Bank

Phase 1. Development: Sharing the Risk to Succeed

The development phase of large solar projects in Africa is a true "valley of death." The time, costs, and risks are extremely high. In the classic model, a single actor – the developer – bears this entire burden alone. They have to self-finance the studies, consultants, and partners, without them genuinely sharing the risk or the potential gain in case of success. It's a highly imbalanced situation that often leads to the project being abandoned.

The FlexUp approach radically changes this dynamic. The goal is to involve and financially incentivize all stakeholders from day one. By allowing everyone to become a partner in the project, we encourage immediate collaboration to accelerate development and optimize its components.

Furthermore, this risk-sharing has a direct impact on the final price of energy. If the developer bears all the initial risk alone, they will logically demand a very high margin in case of success to compensate. This margin weighs on the project's overall economics and results in a higher electricity price for the end consumer.

To give you a concrete example from my experience: in 2015, with my company Canopy, I led a working group with representatives from the energy ministries of the WAEMU countries (West African Economic & Monetary Union). My proposals to accelerate solar power in Africa were already the DNA of FlexUp:

- Finance preliminary studies (grid connection, land, impact) through the state or the national utility.

- Work with open-book business plans, where risks are shared and prices adjust automatically to real costs.

- Implement a standardized contractual framework.

FlexUp is the tool that now makes it possible to implement these principles simply and transparently. The model of that time, which is still too often the norm, is absurd: several developers work in parallel and in competition, financing the same costly studies, only to discover years later that their project is not "bankable." It's a huge waste of time and resources.

With FlexUp, one can even imagine an "umbrella" project that would finance the creation of a standardized framework for an entire region, sharing the risks and benefits of this standardization work among the different states and operators.

Phase 2. Implementation: Aligning Interests to Lower Costs

Once development is complete, the same principle applies to financing, construction, and operation. If the investor is the only one bearing the financial risk, they will set a very high target return on investment to cover all uncertainties, which, once again, increases the price of energy.

The FlexUp system allows for this risk to be distributed with total transparency. The main partner is, of course, the electricity buyer, i.e., the national utility. With FlexUp, we can agree that the price of energy will adapt flexibly to the project's real-time economics.

- For the investor, the risk is reduced, allowing them to offer a much more competitive base price.

- For the national utility, it accepts a portion of the risk but, in return, gets a significantly lower energy price.

In an ideal scenario, we go even further by including other key players in this risk and reward sharing: the constructor (EPC), the operator responsible for maintenance (O&M), and even the banks. When all these stakeholders have their compensation partly tied to the project's profitability, you get exceptional collaboration and much better-managed risk. The final result is:

- A considerably lower price for energy.

- A better risk-return profile for investors.

- Higher profitability for industrial partners, who no longer need to inflate their margins to cover contingencies."

4. How does FlexUp handle critical issues like currency risk or liquidity?

"That's an excellent question because it's precisely one of the major barriers to project financing in Africa, and we offer a very direct solution. For a foreign investor or banker financing in euros or dollars, the return is only real once the funds are repatriated to their home country and currency. The risk is twofold: that the cash gets stuck in the host country, or that the revenues, collected in local currency, lose value due to a devaluation.

The solution we provide with FlexUp is conceptually very simple. We allow for the creation of a reference account for the project in the investor's country and currency – for example, a euro account in France, Switzerland, or the UK.

The fundamental point is this: the project's profitability, which serves as the basis for calculating profit sharing and adjusting the electricity price, is measured solely at the level of this reference account.

In other words, as long as the money remains stuck in the power plant's country or until it has been converted and repatriated in euros to this account, it is not considered a distributable profit for foreign investors.

This solves both problems at once:

- Liquidity and repatriation risk: This risk is no longer borne solely by the investor. It becomes a shared problem for all project partners. If the funds are not repatriated, the financial performance measured in euros is zero, and no flexible compensation is paid. The price of electricity therefore automatically increases (since for the national utility, the final price depends on the rebate on the electricity price, which is part of the flexible compensation). This incentivizes all stakeholders, including local partners, to facilitate the transfer of funds.

- Currency risk: It is automatically integrated and shared. If the local currency devalues, the amount in euros that arrives in the reference account decreases, which mechanically reduces the project's measured profit. The FlexUp system, by its flexible nature, adapts to this reality without any need to renegotiate contracts.

In short, FlexUp doesn't magically make these risks disappear, but it makes them transparent and turns them into a shared challenge. The investor's interest – generating a real return in their own currency – becomes the common interest of all project participants."

5. Can you share a concrete use case (wind, solar, etc.) that illustrates FlexUp's added value?

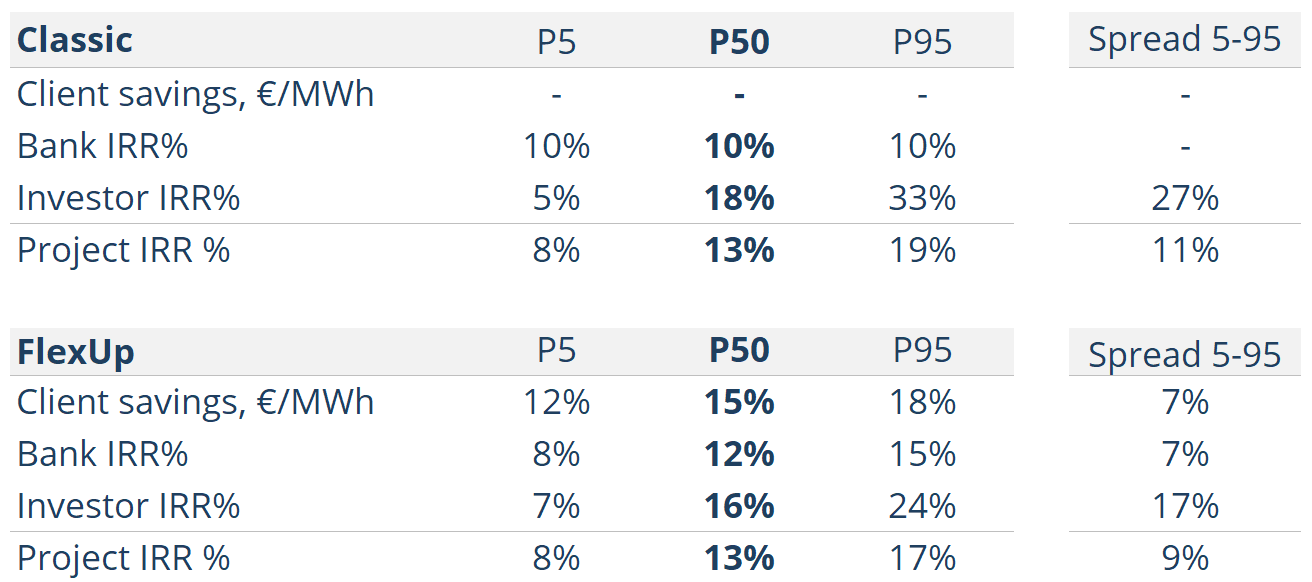

"Absolutely. One of the most telling use cases is the financing of a large solar power plant in Africa. We ran a comparative simulation for a 100 MW solar PV project. This theoretical case perfectly illustrates how FlexUp transforms a high-risk scenario into a win-win opportunity for all partners.

The Classic Scenario: Concentrated Risk

In classic project finance, the risks are very poorly distributed. For our 100 MW plant with a fixed electricity price of €100/MWh, the situation is as follows:

- The bank lends at a fixed 10% rate and takes no risk on the project's performance, as long as its coverage ratios are met.

- The client (the national utility) pays a fixed price of €100, no matter what happens.

- The equity investor bears almost all the risk related to production uncertainties alone.

This concentration of risk creates enormous volatility for the investor. As our simulation shows, their expected internal rate of return (IRR) is 18% in the median scenario (P50), but it can plummet to 5% in a pessimistic scenario (P5) or soar to 33% in a very favorable scenario (P95). That's a colossal 28-point spread, reflecting an extremely high level of risk.

The FlexUp Approach: Shared Risk and Created Value

Now, let's apply the FlexUp model. Our first assumption is that the model, by aligning interests, fosters better collaboration, which translates into an improvement in the project's overall performance. For the simulation, we modeled this as an overall gain of 10% (a mix of increased output, reduced costs and delays, etc.).

In this new framework, the risk is shared, and the results are transformed for each stakeholder:

- For the investor, the benefit in terms of risk-return balance is spectacular:

- Their expected return (P50) drops modestly from 18% to 16%.

- But their risk is significantly reduced: the spread between the pessimistic (7%) and optimistic (24%) scenarios narrows to 17 points instead of 28 in the classic scenario.

- For the bank, it agrees to take on a moderate risk, but its expected return increases significantly, from 10% to 12% in the median scenario. Its IRR fluctuates within a narrow range (from 8% to 15%), which is an excellent trade-off.

- And finally, for the utility and the country, the gain is direct and major: they benefit from an average 15% price reduction on electricity, with very low variation.

Source : Flexup Analysis

The summary above illustrates that the FlexUp scenario is a win for everyone. It's not just a risk-sharing mechanism; it's a system that, by encouraging collaboration, creates additional value that is then shared equitably. The investor reduces their risk, the bank increases its profitability, and the end client pays much less for their electricity.

Beyond Large Projects: Multiple Applications

And this model applies to many other situations in Africa's solar value chain.

Let's take another very concrete example: a solar panel manufacturer wanting to develop its market on the continent. It could form partnerships with local installers or distributors and co-finance their working capital needs, helping them buy more stock and fund their growth.

This financing can be provided as FlexUp credit. By using the FlexUp online application for total transparency, the panel manufacturer gets a return on investment directly linked to its partner's commercial success. In turn, the local partner can accelerate its development, knowing that its supplier is directly invested in its success.

In conclusion, whether it's for financing large infrastructure or for developing commercial partnerships, the principle remains the same. FlexUp transforms client-supplier or investor-project relationships into true partnerships. By aligning financial interests, we don't just distribute risks better; we create the conditions for stronger collaboration, which generates more value for everyone involved."

6. What obstacles are you currently facing in the adoption of this model, especially with traditional banks?

"The main challenge, as with any disruptive innovation, is not so much the complexity of the model but the weight of habit. I would group them into three main obstacles.

The first is simply novelty. FlexUp is a new and still little-known system. Our absolute priority is therefore to communicate, evangelize, and raise awareness of the model and its benefits.

The second obstacle is the need for a conceptual shift. Paradoxically, while the FlexUp model is actually much simpler and more intuitive than the classic system, it requires an effort. Not an effort of understanding, but an effort to "unlearn" the reflexes conditioned by decades of practicing the traditional model.

And that brings us to the third and main obstacle: the inertia of traditional mindsets, particularly among institutional players. Banks, public administrations, large investors, and operators are accustomed to very rigid frameworks: standardized tenders, long-term contracts based on fixed models, etc. Asking them to step out of this "straitjacket" to adopt a collaborative and flexible system is a major challenge. Traditional banks, for example, have risk analysis models entirely calibrated for the classic system; evaluating a project where costs are variable and risks are shared requires a new approach on their part.

Our strategy to overcome these obstacles is therefore pragmatic. We know that the first adopters of FlexUp will likely not be the major institutions, but rather:

- Small entrepreneurs, especially in contexts where the economy is less formal and where flexibility is a condition for survival.

- Innovation players – start-ups, incubators – who are by nature open to experimenting with more agile, alternative systems.

The success of these pioneers will be our best argument. It is by demonstrating the gains in performance, resilience, and profitability through concrete examples that we will then be able to convince more established players of the immense added value of this new model."

7. What is your vision for FlexUp's role in financing Africa's energy transition in the next 5 to 10 years?

My vision is that FlexUp can become a major catalyst for the energy transition in Africa, for one simple reason: Africa is the continent with the most immense needs and where the barriers of the current system are most colossal. It is precisely in this type of environment that an innovation like ours can have the most significant and rapid impact.

Today, Africa's energy challenge is immense. We're talking about an overwhelming dependence on expensive and unreliable diesel generators, a population accustomed to frequent power outages, and entire rural areas with no access to electricity. The need for a rapid transition to renewable energy is therefore an absolute emergency. Yet, the classic financing system, with its rigidity and demands, has simply failed to provide a response commensurate with this pressing need.

This is where FlexUp changes the game. The energy sector in Africa is driven by a new generation of very open-minded players. In general, African entrepreneurs demonstrate incredible resourcefulness and creativity. They are pragmatic. I am convinced that as soon as they see that FlexUp provides concrete solutions to their problems of financing, partnership building, and growth, they will adopt it with surprising speed.

That is why my vision is that Africa will not just be a continent that adopts an innovation. I believe that the energy transition in Africa, powered by models like FlexUp, will become an example for other countries around the world to follow. It will show that it is possible to deploy vital infrastructure in a more agile, more collaborative, and more equitable way, creating a model from which more established countries can in turn draw inspiration.

8. If you had one piece of advice for an African investor or entrepreneur hesitant to engage with an innovative model like FlexUp, what would it be?

"My advice would be very direct and can be summed up in a sentence I have always applied as an entrepreneur: 'The only way to know is to try!'

For an entrepreneur or investor who is hesitant, this is all the more true with FlexUp, because we have done everything to make trying it risk-free and constraint-free.

First, access is free to start. We are offering a 12-month free subscription to our Pro plan for all beta testers. Beyond that, our application remains free for any activity generating less than €5,000 in monthly order volume, and the paid plans that scale with the business start at just €10, then €50. So, cost is not a barrier.

Second, the model is extremely flexible. Adopting FlexUp doesn't lock you into anything. You can start using it for a part of your business while keeping a classic model for the rest. And if, for whatever reason, you want to stop, you retain complete freedom to go back to a 100% traditional model.

So, my advice is simple: try it. It's easy, it's free, and you remain totally free to go back. But most importantly, it will give you the opportunity to intimately understand how the model works. And I am absolutely convinced of one thing: once you see the concrete benefits for your cash flow, for your partners' motivation, and for your agility, not only will you continue to use it, but you will become an ambassador and an evangelist for FlexUp yourself."

To Learn More

To delve deeper into the concepts presented in this article, we invite you to download the complete presentation of our detailed analysis.

If you would like to discuss our approach further or submit a specific project for consideration, please feel free to contact us directly.

About Africa Cleantech Radar

Africa Cleantech Radar gives you a simple and precise overview of Africa's rise as a future global cleantech powerhouse.

In each edition, you will find:

- Essential information,

- The latest funding rounds,

- Sector trends,

- And the ideas shaping the continent's energy and climate future.

Are you an investor, entrepreneur, policymaker, or simply passionate about cleantech in Africa? Subscribe now!

Reinventing Solar Project Financing in Africa